Have employee or more employee meetings on retirement savings aka a 401k meeting. Keep the investing fresh on their minds maybe even monthly inserts with the paychecks. You need more to contribute and more to contribute more.This is what I do as well.

I have an interesting investment problem that just came up again this year. I contribute the max into 401(k). However, at the end of the year when our plan goes through testing we fail on the ratio of contributions from highly compensated to non-highly compensated employees. Therefore, I get money returned to me, both my contributions as well as earnings on those contributions. Its not all of my 401(k) contributions but just a portion. This year its about 24%. That will get reported as income in this tax year and taxed accordingly. This has happened every year for the last three years. I have been taking that money, increasing it by the taxed amount and then putting that into an investment account to try to keep my investments whole but I still loose out on the employer match portion. Interested if this has happened to others and if anyone has a better idea than what I am doing to combat this.

Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Ways to maximize savings for retirement - If you are already maxing out your 401K

- Thread starter npaden

- Start date

npaden

Well-known member

I have clients who maxed out their tax advantaged savings: ie IRA, Roth IRA, 403B's, 401K's etc and now many complain that the government is basically in control of when and how they can take their money out.

I watch my parents who are in their 80's and scrimped and scratched and saved, now they are on positive cash flow just with social security because they don't do much given their health. Seems a better life balance would be in order to do some of the bucket list things now.

I max out too but also am working on building assets and equity outside of the stock market. The market right now seems so juiced on low interest rates, continued FED easy money QE and Trillion dollar deficit spending that it has more downside risk than upside potential IMHO, which is worth zero btw

Just my two cents.

Nemont

For sure some truth to that, although that is one of the big benefits of the Roth IRA is that the distribution requirements are way more relaxed than a 401k. There is no required minimum distributions like there are for a 401k. Also having some $ in the Roth can allow you to maximize tax savings by splitting up withdrawals from a taxable 401k and the nontaxable Roth to get you where you want to be.

For sure it is a good idea to build some assets outside the stock market, I do like being able to grow as much as I can tax free though.

one of the big benefits of the Roth IRA is that the distribution requirements are way more relaxed than a 401k. There is no required minimum distributions like there are for a 401k. Also having some $ in the Roth can allow you to maximize tax savings by splitting up withdrawals from a taxable 401k and the nontaxable Roth to get you where you want to be.

This!

I’m shooting for diversity (pre tax/after tax) to have some knobs to turn during retirement and play the game to minimize tax burden.

Also in the boat of plowing into Roth403b and Roth IRA with the current lower rates. These are set to expire/roll back to previous rates.

Also agree that you need to plan for retirement but not let it become your sole focus beyond enjoying life.

As in all things, plan for the worst, strive for the best, it will end up somewhere in the middle.

A "Backdoor Roth" comes into play for married couples at $193,000 AGI and $122,000 for filing single. Below that you can do a regular Roth. AGI limit bumps up slightly for 2020, and there is a phase out. There is also a "Mega Backdoor Roth" for 401k plans that allow it, common enough that there are a lot of personal finance bloggers and other articles that talk about it, but not available in most 401k plans.

Roth Conversions are another strategy that can work for people that are retiring and have both IRA and after tax investments available for spending to cover the taxes, or having a down income year due to business losses or other activities that will absorb the income. With historically low tax rates some people with high IRA and 401k account balances are trying to get as much converted as possible and paying taxes up to the 24% bracket (321k for 2019) and converting it to Roth. Good problem to have.

Some info from a random blog I found on google, has screenshots for using a Vanguard IRA: https://www.physicianonfire.com/backdoor/

Thank you!

npaden

Well-known member

I just found out about the "Mega" Backdoor Roth. Anyone using one? I have some control over our 401k plan and am thinking about checking into it for our plan.

thecollegeinvestor.com

thecollegeinvestor.com

Understanding The Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is a strategy to leverage after-tax 401k contributions as a way to boost Backdoor Roth IRA conversion dollars.

thecollegeinvestor.com

Slate

Well-known member

- Joined

- May 23, 2020

- Messages

- 208

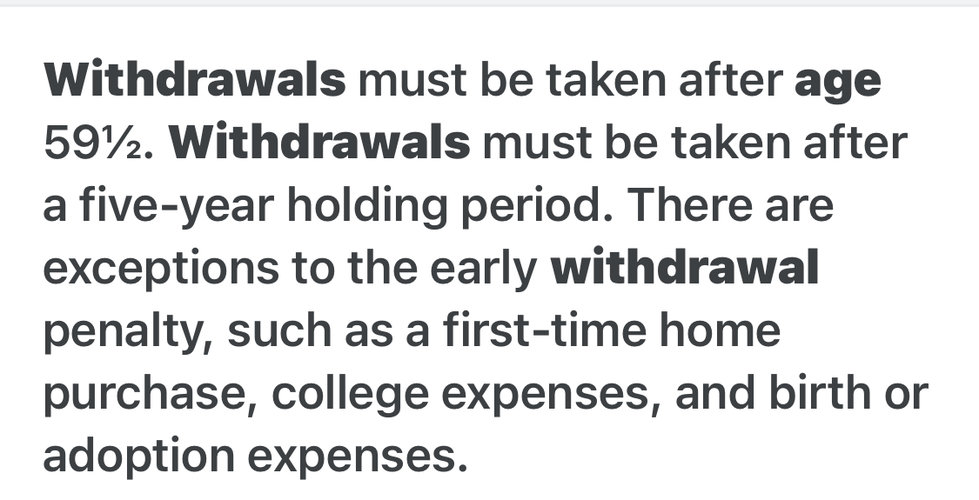

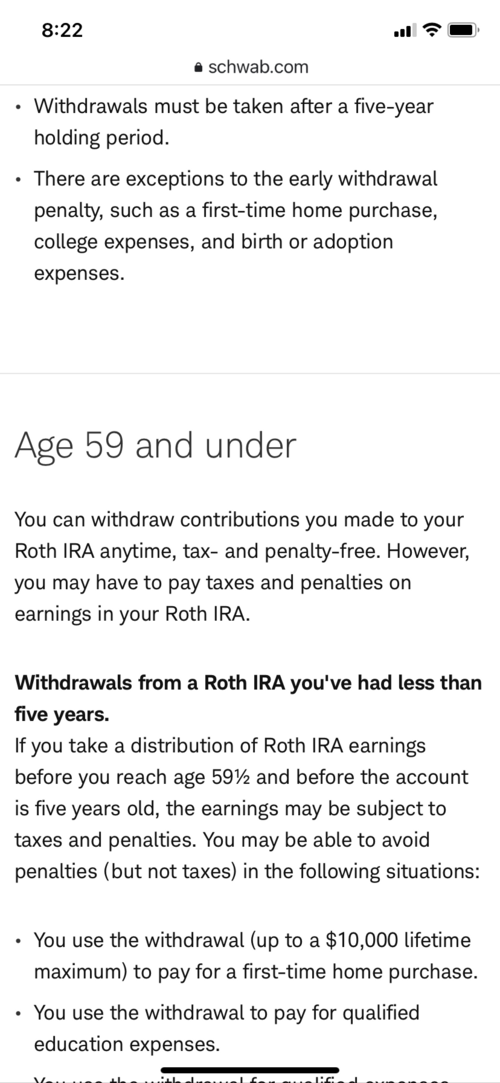

My only issue is the age restrictions. I am retiring next March at 48. I want access to my money while young and able. That’s just me. But it is great advice.

timberman56

Active member

anyone using a self-directed ROTH for real estate transactions ? if so, any bad experiences?

i believe you can pull any of your contributions out of a roth at any time without penalty. kind of defeats the purpose of putting it in there, but it’s a nice option if needed.My only issue is the age restrictions. I am retiring next March at 48. I want access to my money while young and able. That’s just me. But it is great advice.

That does sound interesting. never heard of the mega backdoor roth. i guess when i get to the point where my wife and i have our backdoor roths and roth 401ks maxed out and the house is paid off it may be worth looking at.I just found out about the "Mega" Backdoor Roth. Anyone using one? I have some control over our 401k plan and am thinking about checking into it for our plan.

Understanding The Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is a strategy to leverage after-tax 401k contributions as a way to boost Backdoor Roth IRA conversion dollars.

Slate

Well-known member

- Joined

- May 23, 2020

- Messages

- 208

i believe you can pull any of your contributions out of a roth at any time without penalty. kind of defeats the purpose of putting it in there, but it’s a nice option if needed.

Attachments

westbranch

Well-known member

My only issue is the age restrictions. I am retiring next March at 48. I want access to my money while young and able. That’s just me. But it is great advice.

There is an option to take "substantially equal period payments" out of IRAs, a lot of early retirement blogs talk about the process if you do a little searching online.

Substantially equal periodic payments | Internal Revenue Service

Insights into substantially equal periodic payments under IRC section 72(t)(2)(A)(iv), with examples.

Slate

Well-known member

- Joined

- May 23, 2020

- Messages

- 208

It’s definitely not a bad thing. If you are saving for retirement it’s a good option. I’m definitely in the situation where I’m all maxed out on my 457. I am short as far as time till retirement.

westbranch

Well-known member

I just found out about the "Mega" Backdoor Roth. Anyone using one? I have some control over our 401k plan and am thinking about checking into it for our plan.

Understanding The Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is a strategy to leverage after-tax 401k contributions as a way to boost Backdoor Roth IRA conversion dollars.

I know more than a handful of people using them. Works well for those that have the income and ability to save. My understanding is that it can be harder for small company's add the provisions needed to their 401k plan documents due to all of the testing provisions.

just curious, what are your retirement plans? i aspire to be an early retiree as well, though im sure i’ll never be fully retired. my mind doesn’t rest for more than a minute so i need something to keep me busy. Hopefully by that time ill own some income producing properties to keep me busy.It’s definitely not a bad thing. If you are saving for retirement it’s a good option. I’m definitely in the situation where I’m all maxed out on my 457. I am short as far as time till retirement.

Slate

Well-known member

- Joined

- May 23, 2020

- Messages

- 208

My retirement to be honest is to relax, vacation with my wife and hunt. I’m very active as far as doing a lot of hiking and outdoor activities. I don’t need work to keep me busy and I definitely have a spending plan for retirement. I want to spend more of my money while young and able. One life to live. I have no problems spending money when I want things. I have been responsible through the years. Paid off my house and have no credit card debt. It’s key to an early retirement for an average person. Having no debt is freedomjust curious, what are your retirement plans? i aspire to be an early retiree as well, though im sure i’ll never be fully retired. my mind doesn’t rest for more than a minute so i need something to keep me busy. Hopefully by that time ill own some income producing properties to keep me busy.

Last edited:

npaden

Well-known member

Thanks. I don't think they are very common. Our 401k plan guy hadn't heard of them and I audit 401k plans and hadn't heard of them. We do the safe harbor for our plan so we don't have to pass the discrimination testing so that for sure helps.I know more than a handful of people using them. Works well for those that have the income and ability to save. My understanding is that it can be harder for small company's add the provisions needed to their 401k plan documents due to all of the testing provisions.

I think I am going to continue to push it with our 401K plan administrators. I still have 10 years or so before retirement so I should be able to get a little tax free growth out of it, and hopefully there will be some of it that will be in there a whole lot longer than 10 years as I will be trying to structure my withdrawals to maximize the tax rate brackets as it comes out. There are a couple other folks here that are maxing out their 401k but I think only a couple of of us are even doing the regular backdoor Roth IRA.

I do the backdoor Roth IRA for both my wife and I and we now are both over 50 so we can do $7,000 each. I think including employer match I could do another $20,000 with the Mega backdoor Roth option through my 401k. I maybe able to even leave it inside our 401k Plan since we have a Roth option available.

Seems like a bit of work to get it done, but $20K times 10 years and hopefully another 10 years or so of earnings on that would be worth messing with.

Doubleplay

New member

- Joined

- Feb 11, 2021

- Messages

- 18

I agree the market is way overpriced and not at a good entry point. However because of no other alternative for most people and funds, it can keep going like this for a while.I have clients who maxed out their tax advantaged savings: ie IRA, Roth IRA, 403B's, 401K's etc and now many complain that the government is basically in control of when and how they can take their money out.

I watch my parents who are in their 80's and scrimped and scratched and saved, now they are on positive cash flow just with social security because they don't do much given their health. Seems a better life balance would be in order to do some of the bucket list things now.

I max out too but also am working on building assets and equity outside of the stock market. The market right now seems so juiced on low interest rates, continued FED easy money QE and Trillion dollar deficit spending that it has more downside risk than upside potential IMHO, which is worth zero btw

Just my two cents.

Nemont

KU_Geo

Active member

My wife and myself both have this option and take advantage of it. We do pretax contributions, which automatically shut off at the IRS limit for the year (think it’s $19500 for 2021), and out plan automatically continues our contribution % as after tax. we continue to get the company match and the combine limit of my contribute and match is $58k for the year. One thing to note is if your plan allows in service distribution or not. If yes, you can convert after tax to Roth every year, which does trigger some tax on aftertax gains. If your plan does not offer in service, you simply wait until you leave the company and then roll all pretax, match, and All gains into a traditional IRA, and then after tax contributions into a Roth IRA. This does not trigger a taxable event. In service conversion is a little less simple but there is an advantage To it as you get money in Roth faster.I just found out about the "Mega" Backdoor Roth. Anyone using one? I have some control over our 401k plan and am thinking about checking into it for our plan.

Understanding The Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is a strategy to leverage after-tax 401k contributions as a way to boost Backdoor Roth IRA conversion dollars.

Similar threads

- Replies

- 22

- Views

- 2K

- Replies

- 49

- Views

- 4K

- Replies

- 123

- Views

- 7K